ON-387: Ethereum 🦄

Apr 24, 2026

📝 Editor's Note:

Welcome back! This is the first issue of OurNetwork since our reboot announcement.

And what better way to get in the groove than covering Ethereum, the blockchain which leads crypto with over $46.8B in total value locked. Even after a wild week which had users pulling billions from Ethereum-based protocols, the chain accounts for 53.9% of TVL across all of crypto.

Ethereum's been in a strange place since 2021. On one hand, the ecosystem is succeeding: Layer 2s' aggregate daily transactions are well over 10 times mainnet, stablecoins on the chain are at an all-time high, as Ethereum has pulled off a series of significant upgrades.

On the other hand, ETH's price is over 50% off its all time high, raising persistent questions about whether the asset can sustainable capture value. More broadly too, AI has taken the spotlight as the frontier digital technology, leaving blockchain systems with less of a hype-driven valuation premium.

Before we get into the details however, we're happy say that we're again collaborating with ETHGlobal, which hosts crypto hackathons, on this issue. The organization has sourced 1,200 projects via those hackathons in the last five months with the top verticals being DeFi, at roughly 43%, AI, at 13%, and payments, at 12%. Over 70% of those projects launched on Ethereum or its Layer 2s.

ETHGlobal gearing up for ETHConf, a 5,000-plus person conference featuring speakers like Aave's Stani Kulechov, Uniswap Labs' Hayden Adams, and more. That's in June in NYC — click here for more info.

With that, let's get into it.

– ON Editorial Team

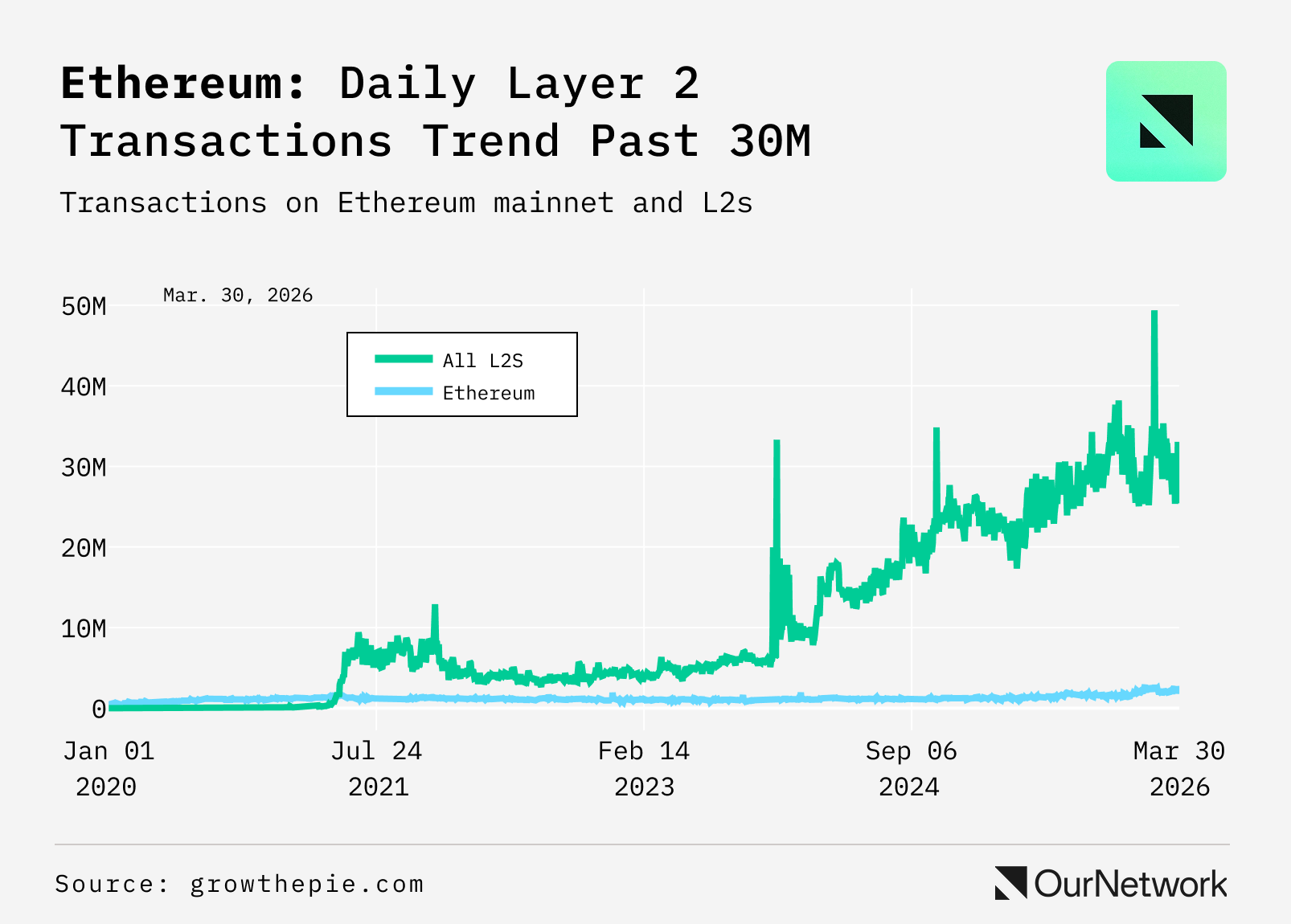

- Ethereum is the dominant Layer 1 in crypto, accounting for 53.9% of all total value locked as of April 2026 and serving as the settlement layer for the majority of onchain stablecoin supply. A defining dynamic of its ecosystem is its Layer 2s — chains that execute transactions off Ethereum before settling them permanently back on mainnet. As of March 30, 2026, L2s process roughly 25-30M daily transactions per growthepie against mainnet’s ~2-3M, a gap of roughly 10x that has widened every year since mid-2021.

Polygon's proof-of-stake chain is not technically an L2 as its transactions don't settle on Ethereum's mainnet. It is included in this transaction count per growthepie's methodology.

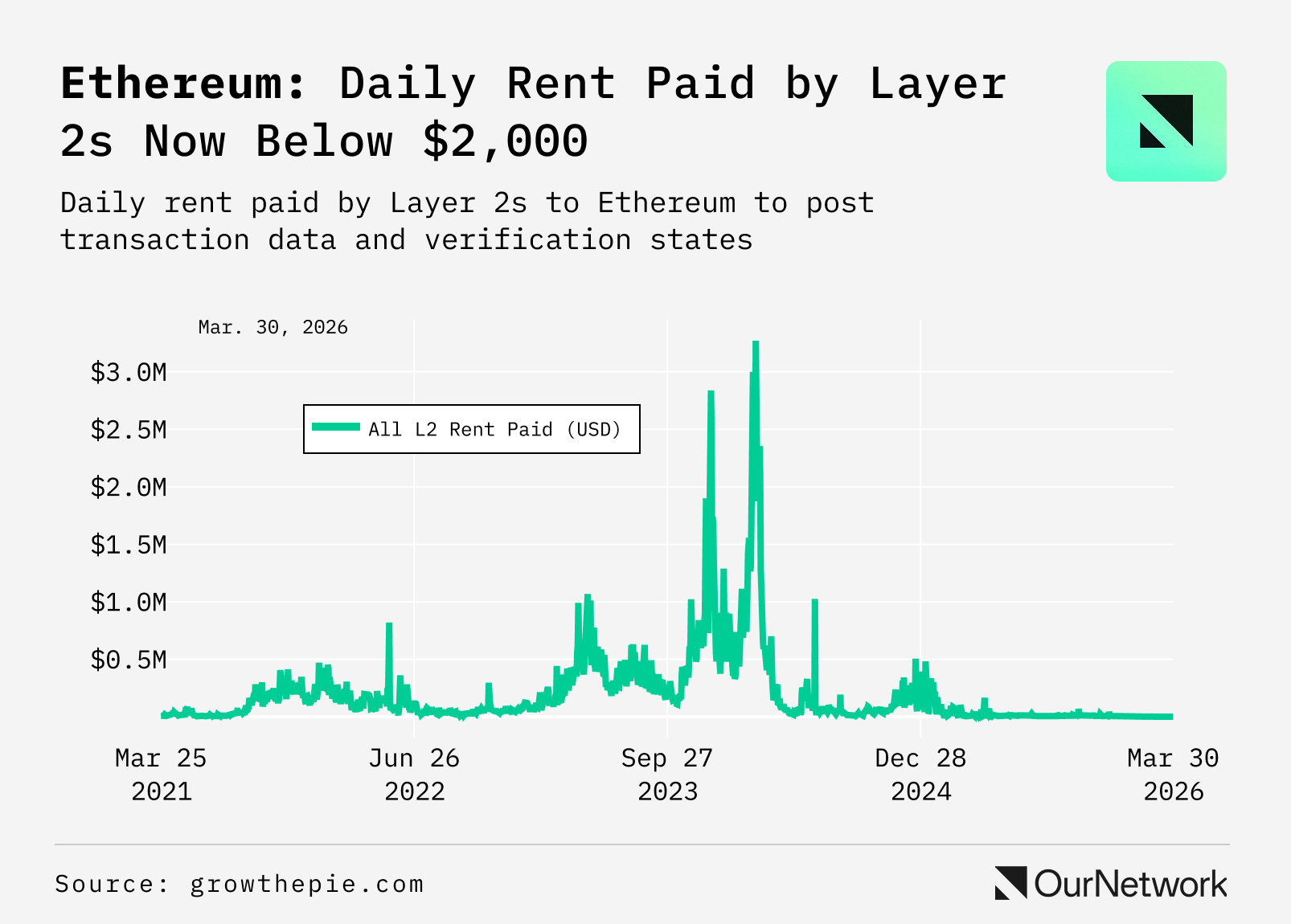

- Notably, while L2 transaction count has continued to grow, the fees those scaling solutions pay to Ethereum’s mainnet have not. This is due in large part to a 2024 upgrade called Dencun, which created a market designed specifically for L2s to post data to Ethereum. This dropped costs for L2s using Ethereum’s base layer as an anchor chain, but also lowered the chain’s revenue from scaling solutions — from a late-2023 peak of approximately $3.0M in daily rent paid to below $2,000 per day by March 30, 2026, a decline of over 99% per growthepie. On its face, this significant short-term drop in revenue appears to be a negative development for the network, but lower settlement costs have transformed Ethereum into a far more viable foundation for L2s long-term.

- Ethereum L2s have been successful in creating one of the most active ecosystems in crypto, with $46.8B in total value locked and 53.9% of all crypto TVL as of April 2026. Fees are no longer prohibitively expensive on either L2s or Ethereum. However, mainnet’s fee channel from its scaling layer has not recovered — blob rent has not sustained any multi-month recovery above $1M/day across the two years since Dencun per growthepie — leaving open the question of whether Ethereum can re-establish durable L1 revenue as its ecosystem continues to grow.

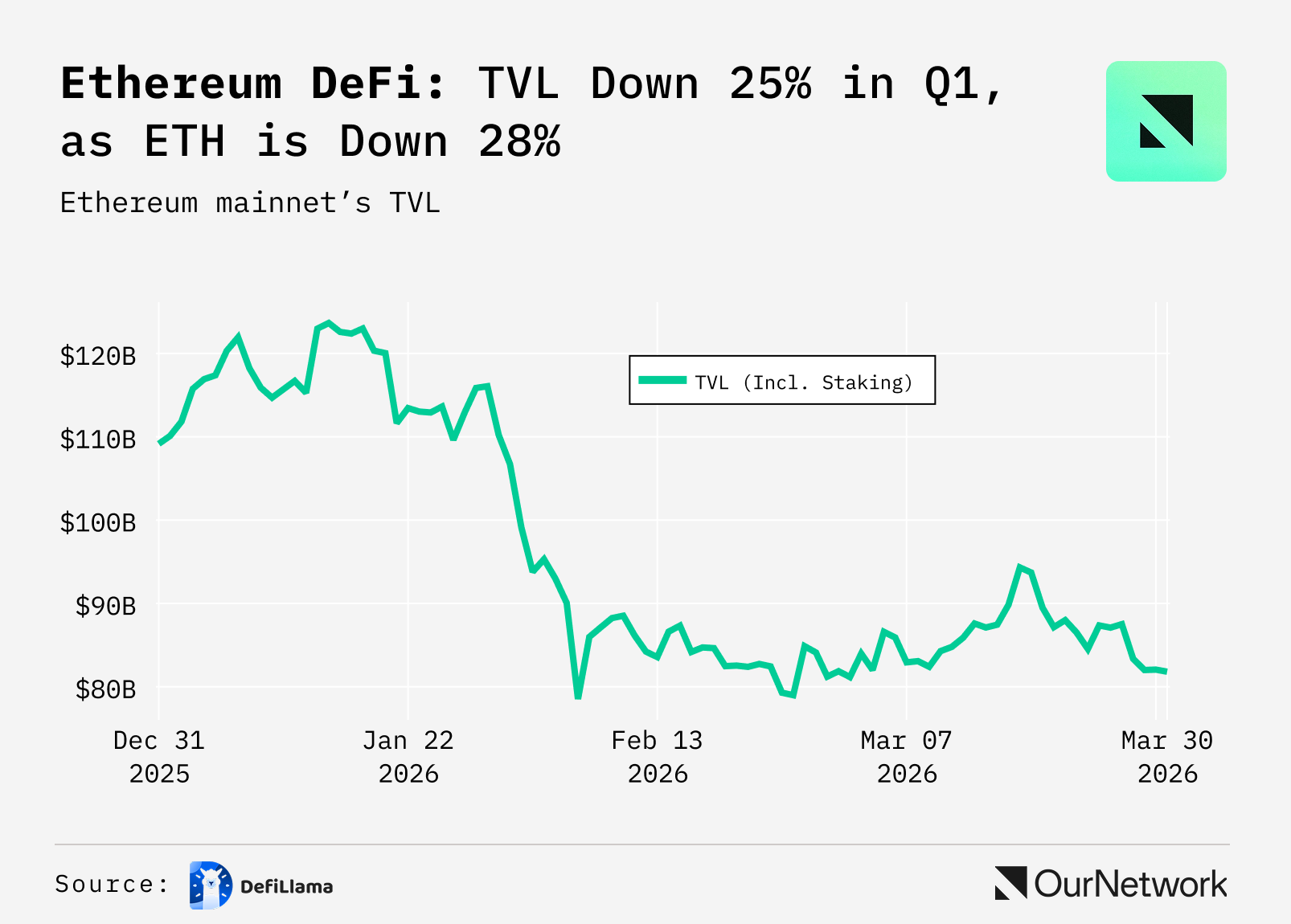

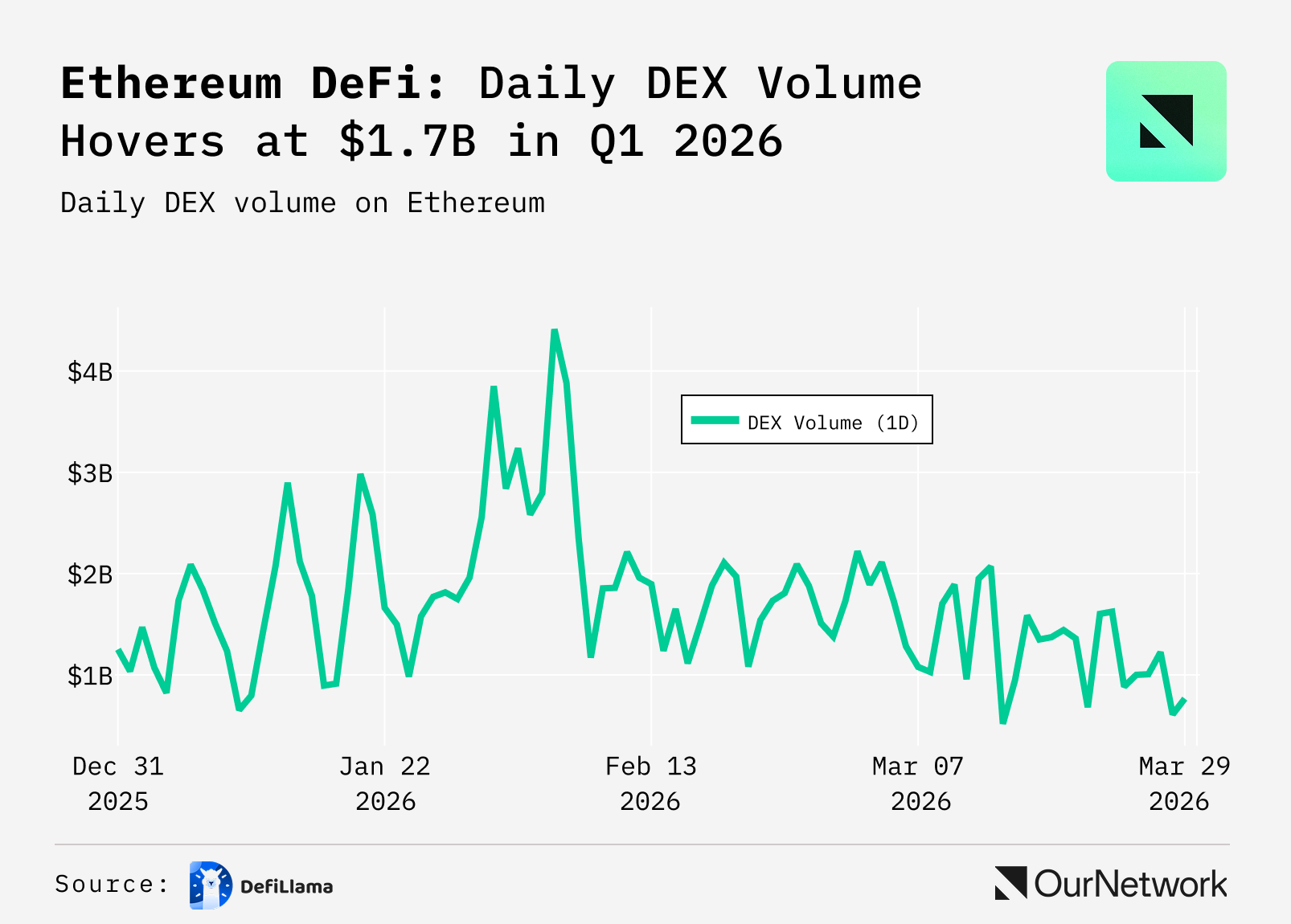

📈 Ethereum DeFi TVL crashed -36.5% in Q1 and came back structurally intact, supported by lending and liquid staking

- Ethereum DeFi TVL peaked at $123.6B on Jan. 15, then collapsed -36.5% to $78.5B by Feb 6, in just 22 days. Single-day DEX volume hit $4.41B on Feb 5, its cycle high, precisely as TVL bottomed. That's not organic selling, but rather forced liquidations. Since then, TVL has recovered to ~$96B with no equivalent volume spike, suggesting deliberate re-entry by larger capital, not retail momentum chasing a bounce.

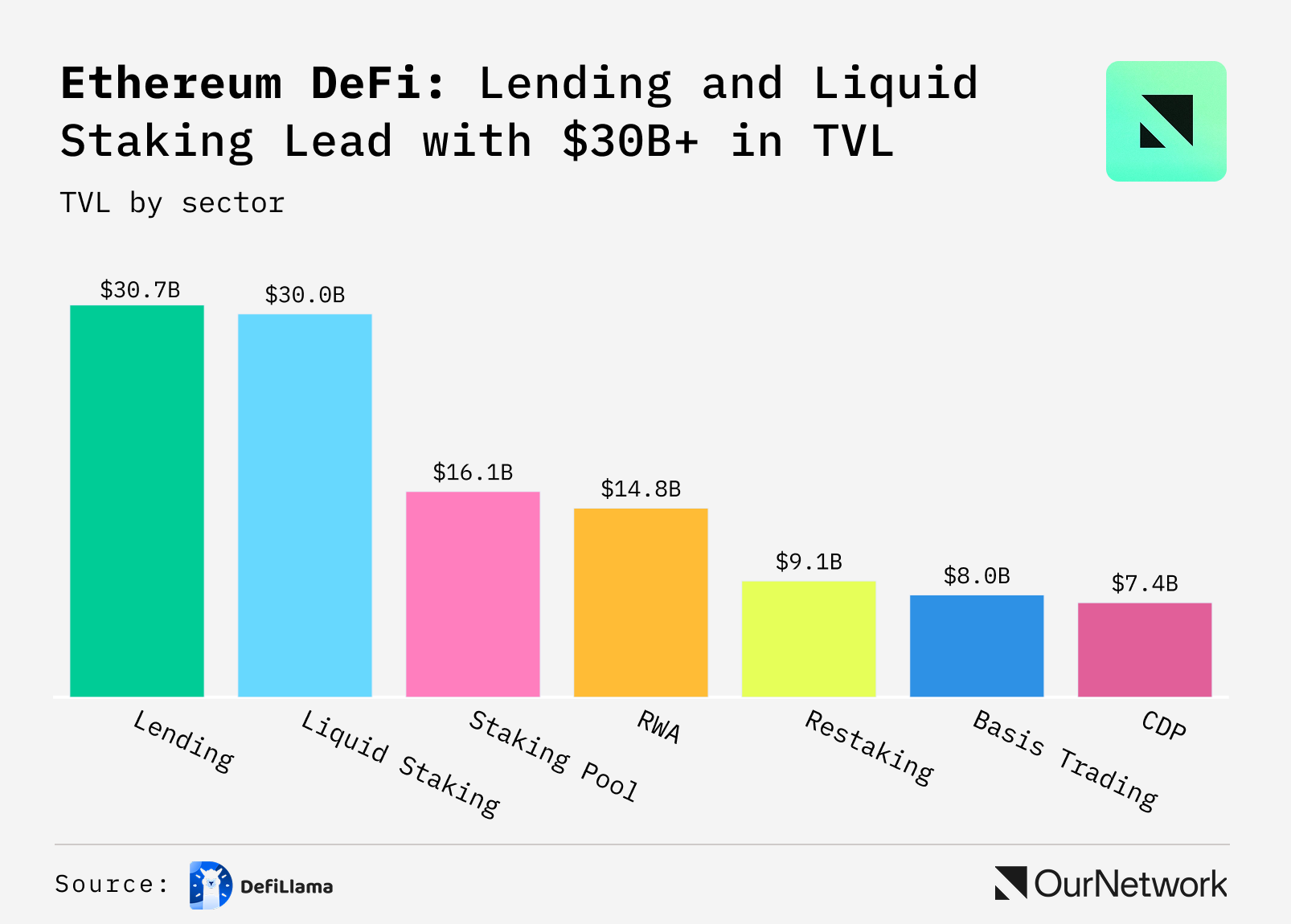

- At $30.7B and $30.0B respectively, lending and liquid staking, are virtually tied as Ethereum's two dominant DeFi categories, separated by just $700M. Together they represent the structural floor of Ethereum DeFi. Behind them, RWA, at $14.8B, and restaking, $9.1B, have grown to $24B combined.

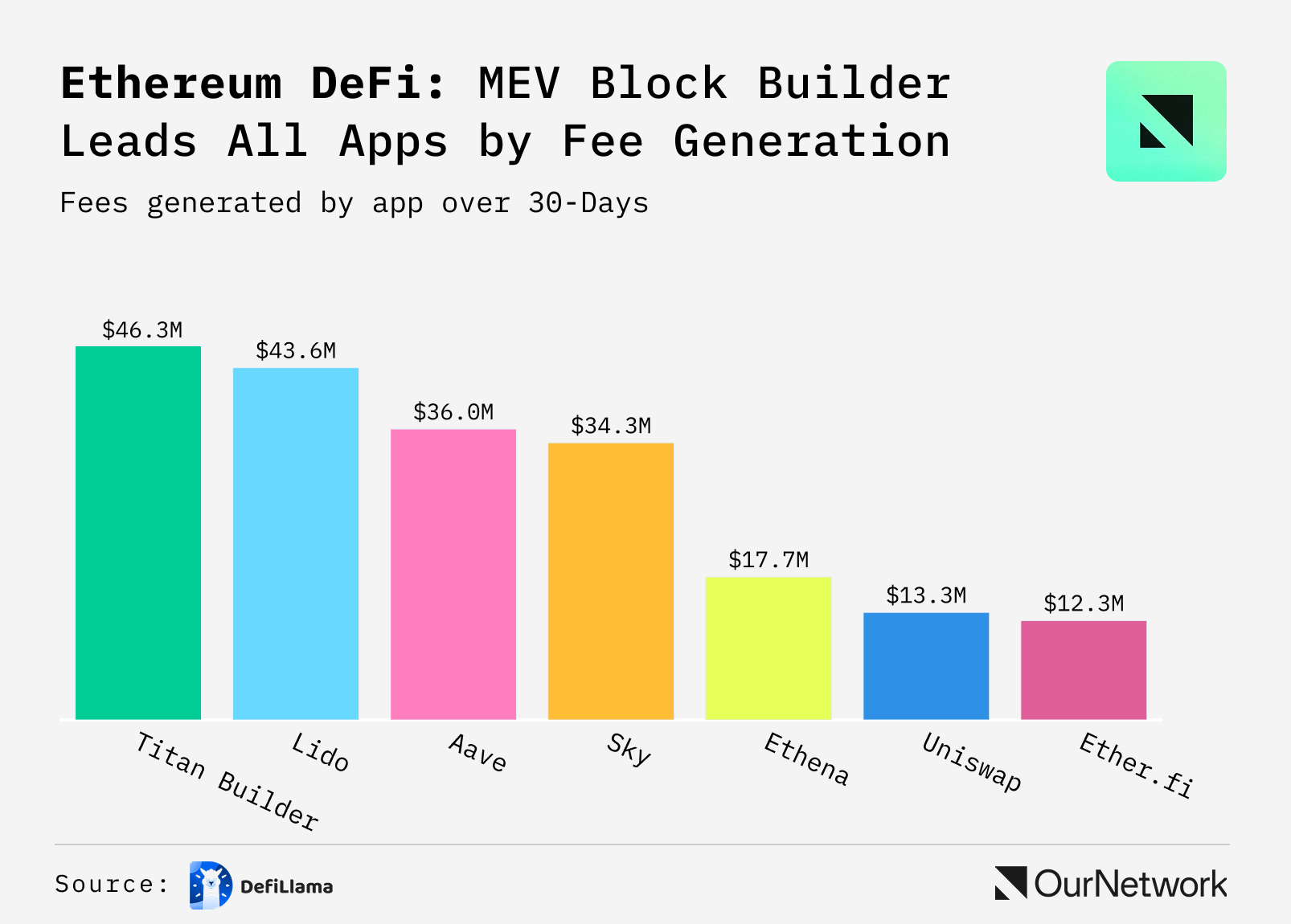

- Surprisingly, the number one fee earner on Ethereum isn't a household DeFi protocol like Aave, Lido, or Uniswap. It's actually Titan Builder, an MEV block builder: $46.3M in fees, up 105% month-over-month, at 85.6% margin. Among user-facing apps, Uniswap dominates spot DEX at $19.9B in 30-day volume while Sky leads on revenue efficiency at 44% margin versus Aave's 13.9%.

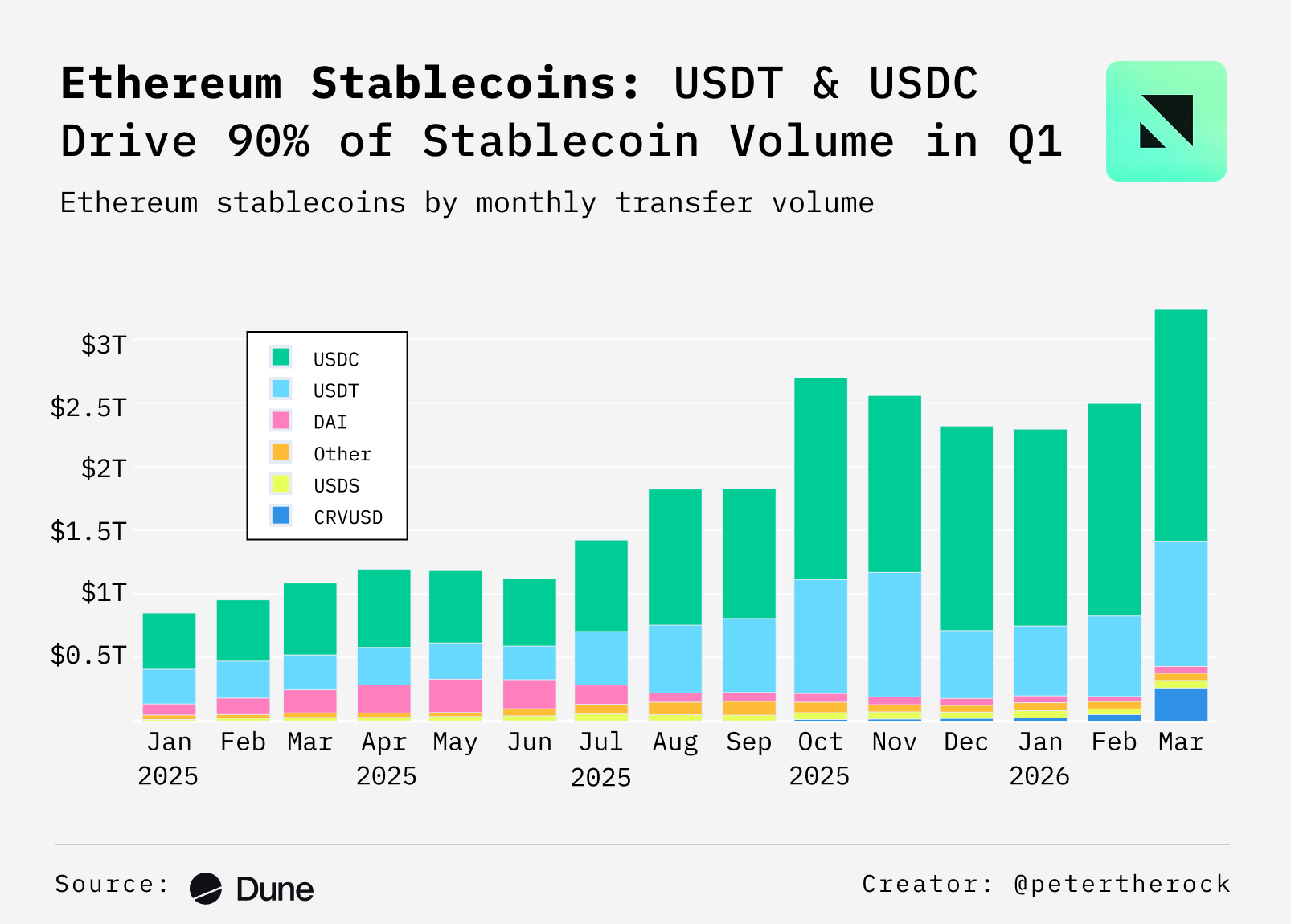

📈 Ethereum’s USD-based stablecoin activity is surging, while supply grows more gradually, signaling stronger real usage across the network

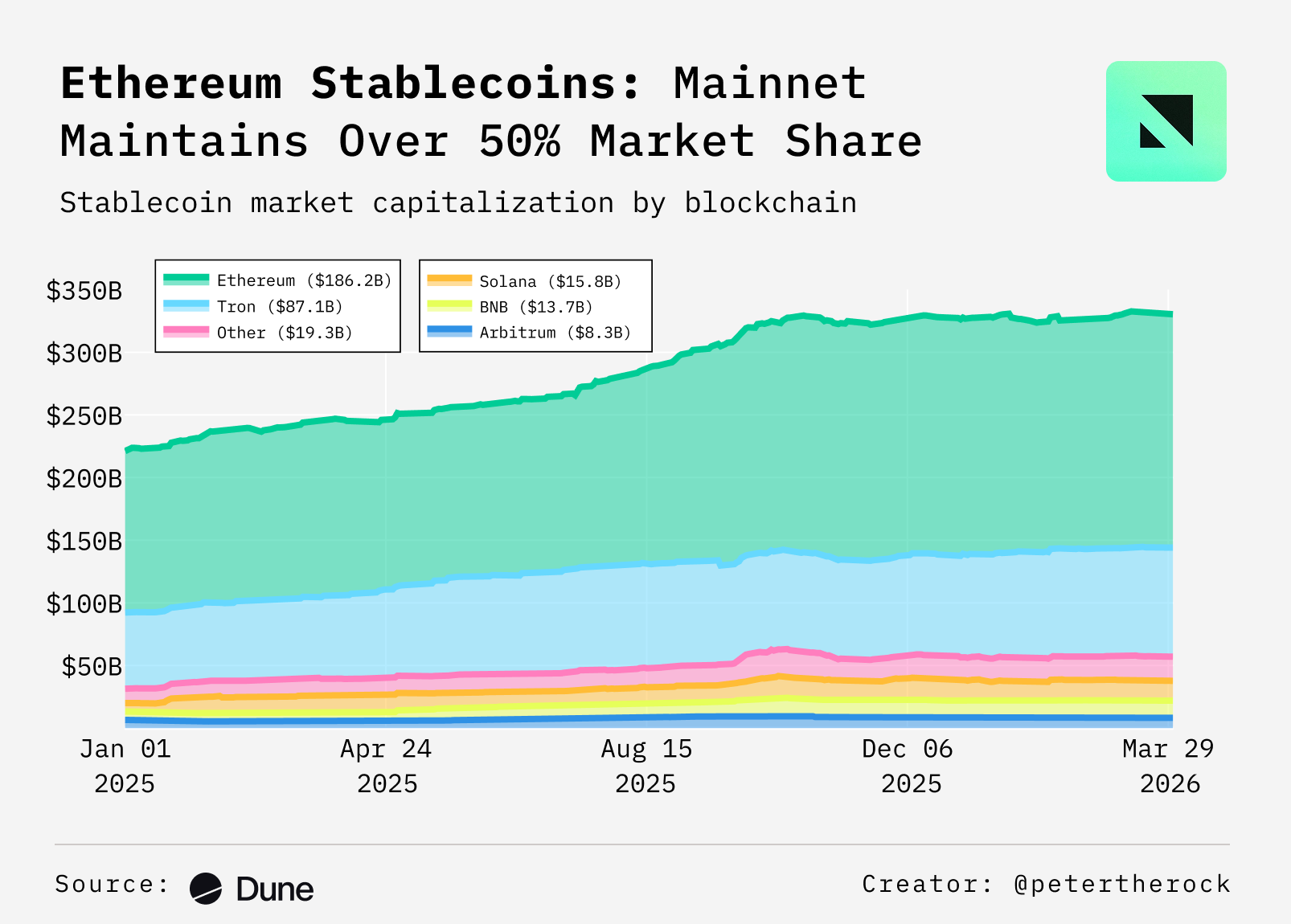

- Ethereum's USD-based stablecoin supply has grown from $130B at the start of 2025 to about $186B today, marking about 45% in year over year growth. Ethereum remains the primary settlement layer for stablecoins, accounting for ~56% of total USD-based stablecoin supply across chains despite rising competition from other networks.

- In March, Ethereum's USD stablecoin activity surged 30% month over month to hit an all-time high. USDC and USDT, which together account for 86.7% of volume, have been driving the growth, reinforcing their dominance as the core settlement assets.

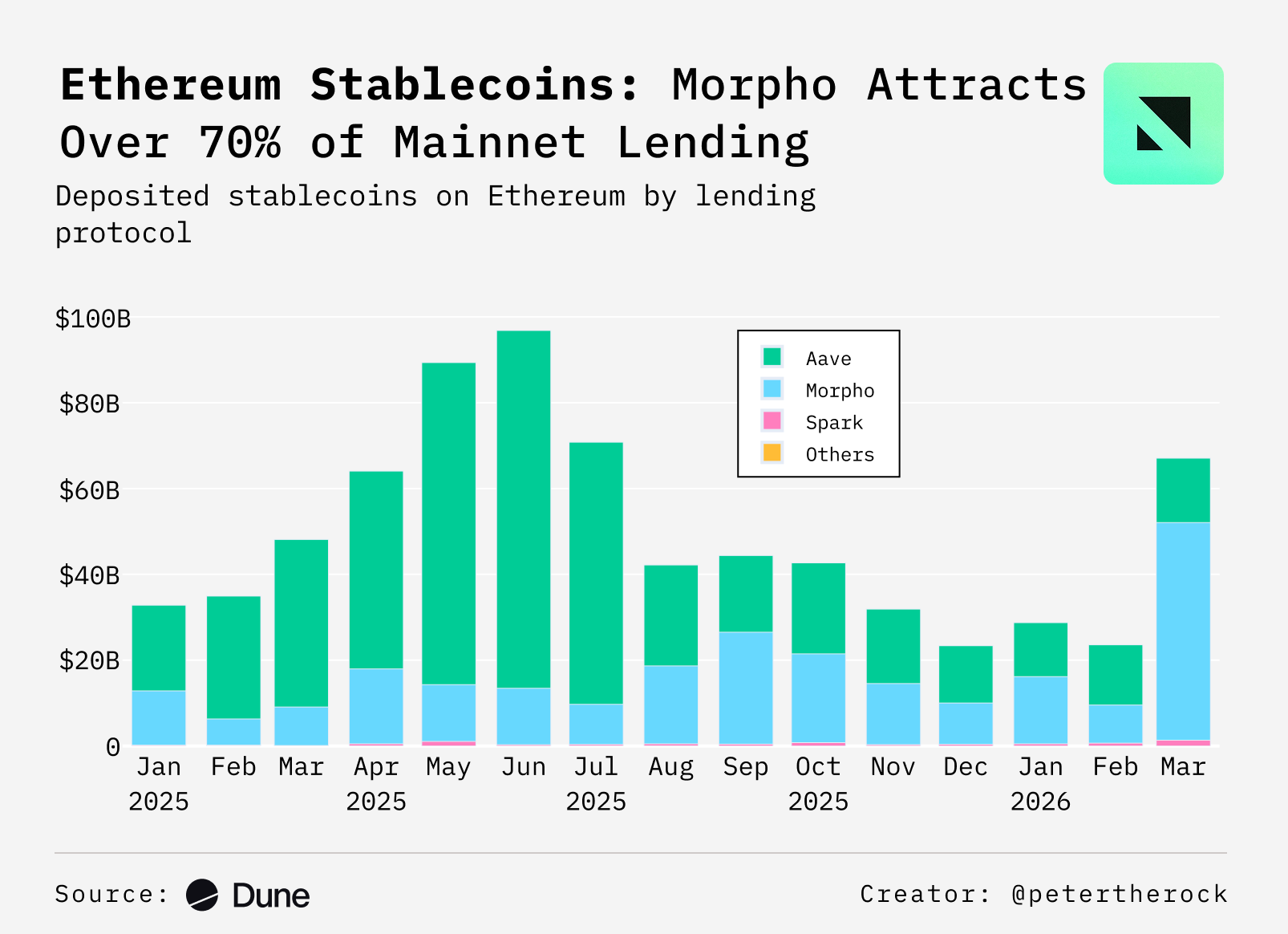

- On Ethereum, stablecoin lending supply volumes tripled month over month to $67B, marking a sharp surge in activity since mid-2025s. Morpho led the growth, accounting for ~75% of volumes, and has now overtaken Aave as the largest lending protocol on the network.

In closing, Ethereum post-hype era is clearly underway. Interest in crypto has waned relative to AI, but there's definitive onchain growth demonstrated onchain in terms of activity and transactions.

And a last plug for ETHConf, coming up in June.

Until next time.