ON-385: Aggregators 🔄

Coverage on Jupiter, Summer.fi, KyberSwap

Jan 16, 2026

📝 Editor's Note:

Welcome to OurNetwork's latest.

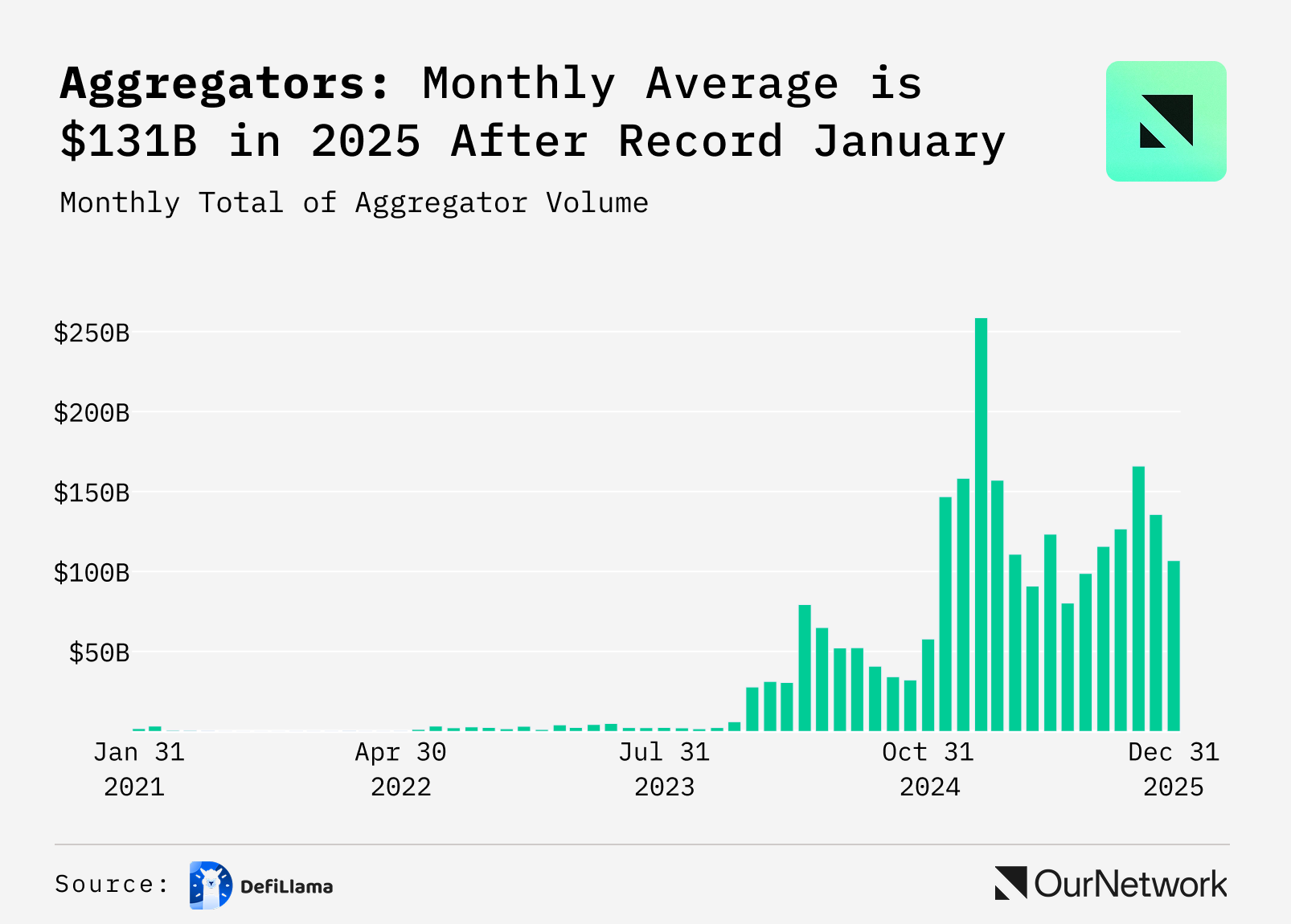

In this one, we're checking out aggregators, a sector whose monthly volume average doubled to $131B per month in 2025 after hitting a $65B monthly average in 2024.

Shoutout to Surf Query, Summer.fi, and Diego for covering some of the biggest players in the space in this one.

– ON Editorial Team

Jupiter | Summer.fi | KyberSwap

👥 Surf Query | Website | Dashboard

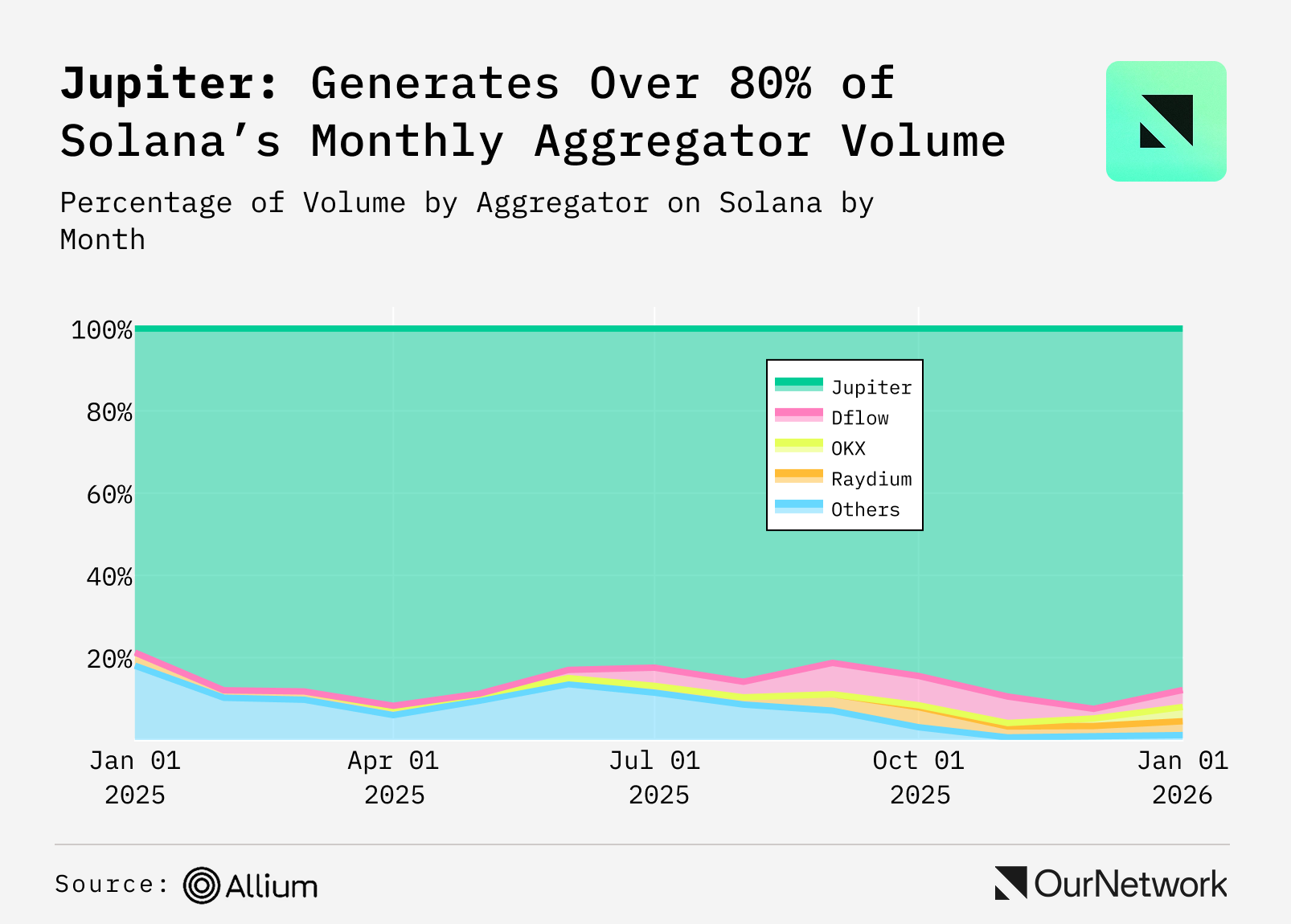

📈 Jupiter is Solana’s Largest Protocol, Controlling ~90%+ of DEX Aggregation and Leading the Ecosystem with Novel Trading Features

- Jupiter is Solana’s leading liquidity and trading layer, with $2.84B in TVL, the largest among all Solana protocols. It consistently routes billions of dollars each month, peaking above $120B in monthly volume in late 2025, cementing its role as Solana’s primary liquidity router. Jupiter handles the vast majority of DEX aggregator volume—often over 80–90% of routed trades. Its 30-day volumes are typically 10–15× larger than competitors, showing how concentrated swap routing is on Jupiter’s rails.

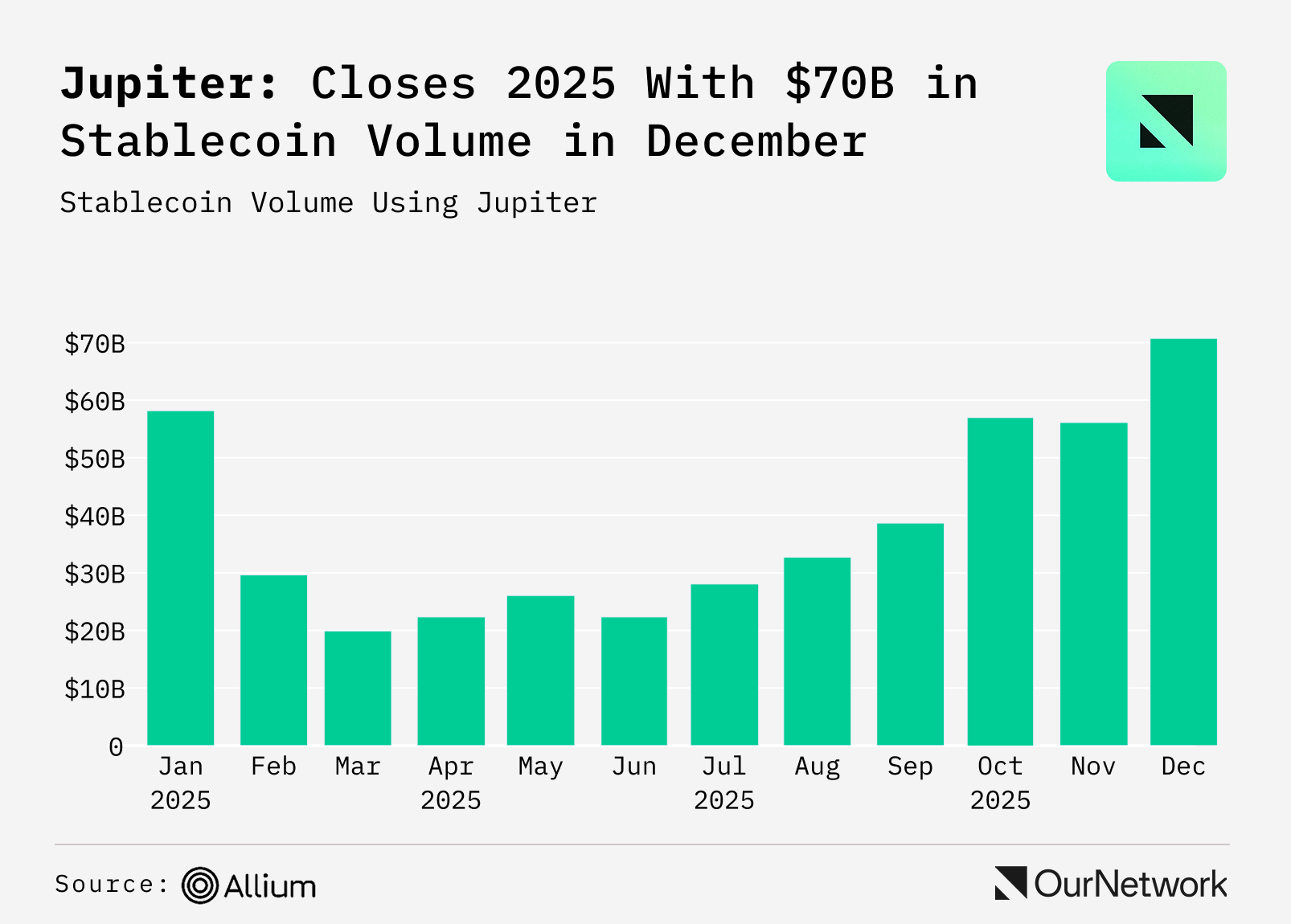

- In 2025, Jupiter grew into the backbone of stablecoin DEX aggregation, processing $461B in volume. Momentum peaked in December with a record $70B month. Average stablecoin monthly volume reached $36B, growing ~6% month-over-month, as Jupiter captured over 90% of the market.

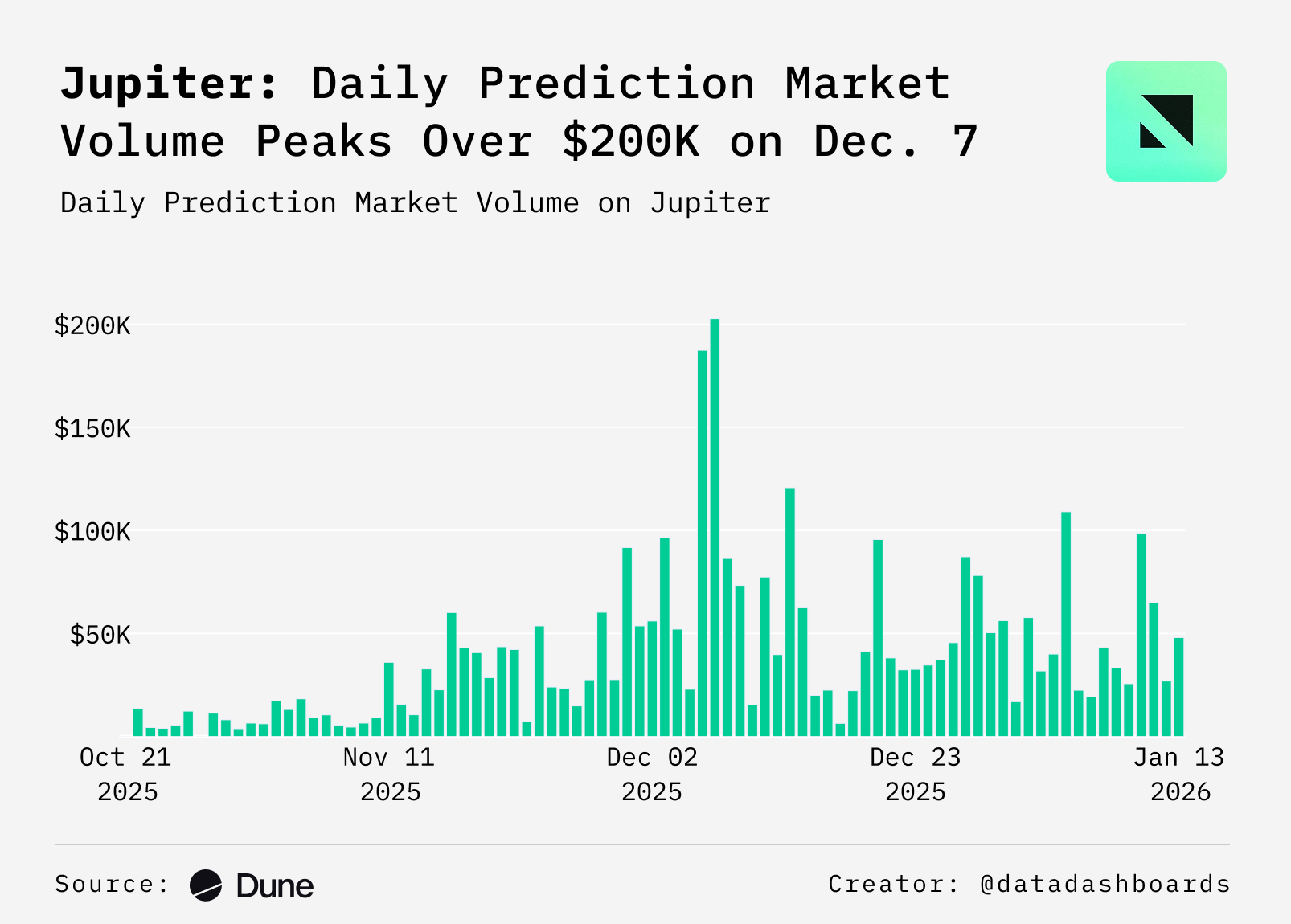

- Beyond aggregation, Jupiter is also expanding into prediction markets, powered by Kalshi. Just three months after launch, the platform has already generated over $3.3M in prediction market volume, alongside a growing TVL of $451K, signaling early traction & user demand beyond spot trading and swaps.

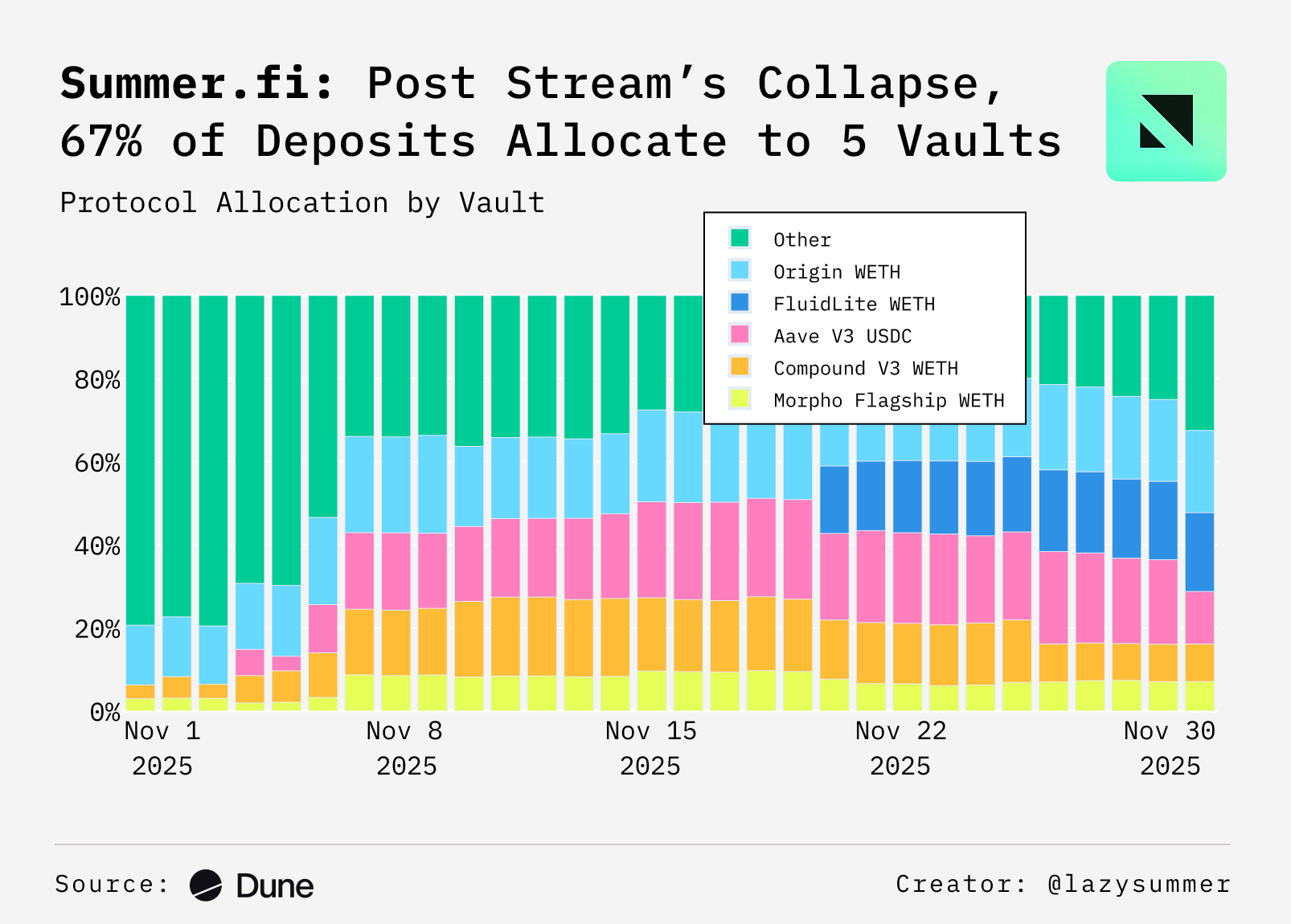

📈 Lazy Summer Continuously Monitors and Reallocates Capital Across Top DeFi Protocols, Ensuring Users Earn the Best Available Yields

- Lazy Summer is a DeFi vault aggregator that automates the highest quality yield sources. It combines expert risk management (via Block Analitica) with automated rebalancing. The system uses two types of actions: Rate Enhancement moves capital to better yields, while Fund Withdrawal reduces exposure when risks rise. Users deposit once and let the protocol optimize, earning more during opportunities and de-risking when market conditions worsen.

- November highlights Lazy Summer's risk-on/risk-off nature. Users access top DeFi yields when risk/reward favors it, reverting to safety when it doesn't. The chart shows automated rebalancing in action, moving from risk-on positions to concentrated bluechip strategies after Stream Finance's collapse.

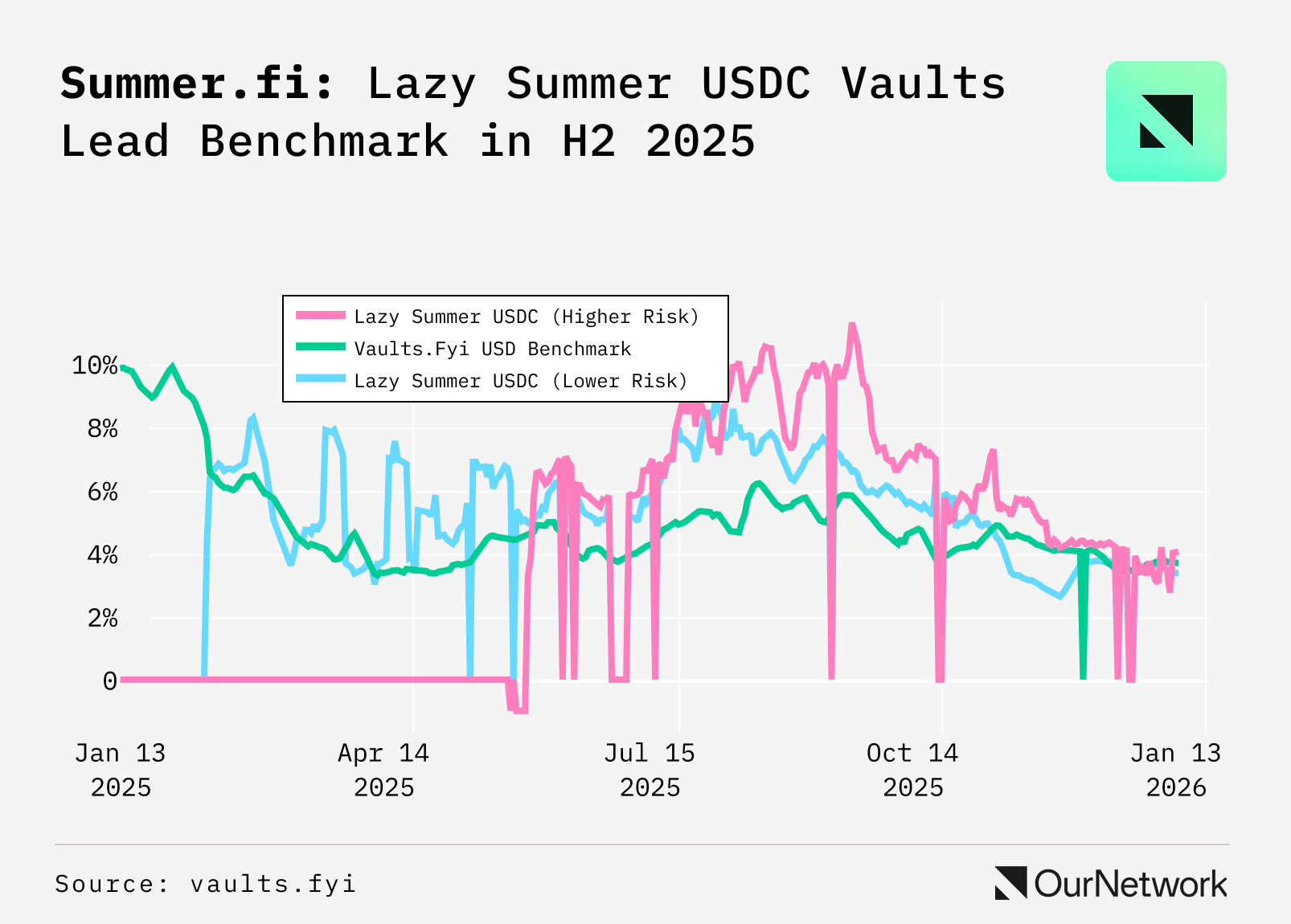

- The test of any yield aggregator is performance during critical moments: protecting capital in extreme stress while delivering safe yields, and capturing significant returns above benchmarks during market excess. Lazy Summer's yield data on vaults.fyi shows it works when it matters most.

🔦

Transaction Spotlight:

This was an automated Rate Enhancement rebalance by the protocol. The system moved 100 ETH from the Morpho Moonwell Flagship pool to Aave V3 to capture a higher yield. This occurred within the "Lower Risk ETH" vault, automatically optimizing the vault's net yield, and users' return, without requiring manual action.

This was an automated Rate Enhancement rebalance by the protocol. The system moved 100 ETH from the Morpho Moonwell Flagship pool to Aave V3 to capture a higher yield. This occurred within the "Lower Risk ETH" vault, automatically optimizing the vault's net yield, and users' return, without requiring manual action.

👥 Diego Cabral | Website | Dashboard

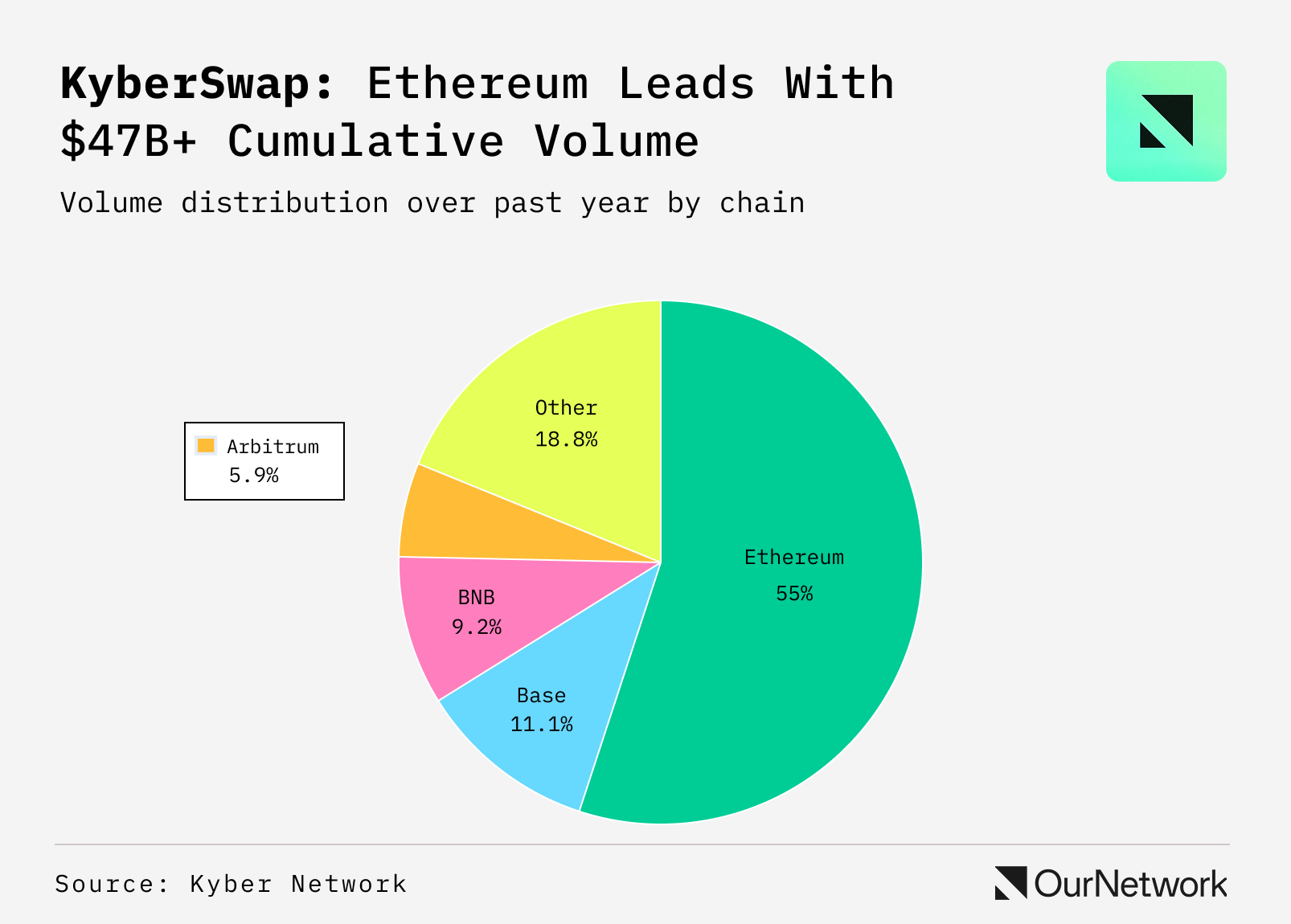

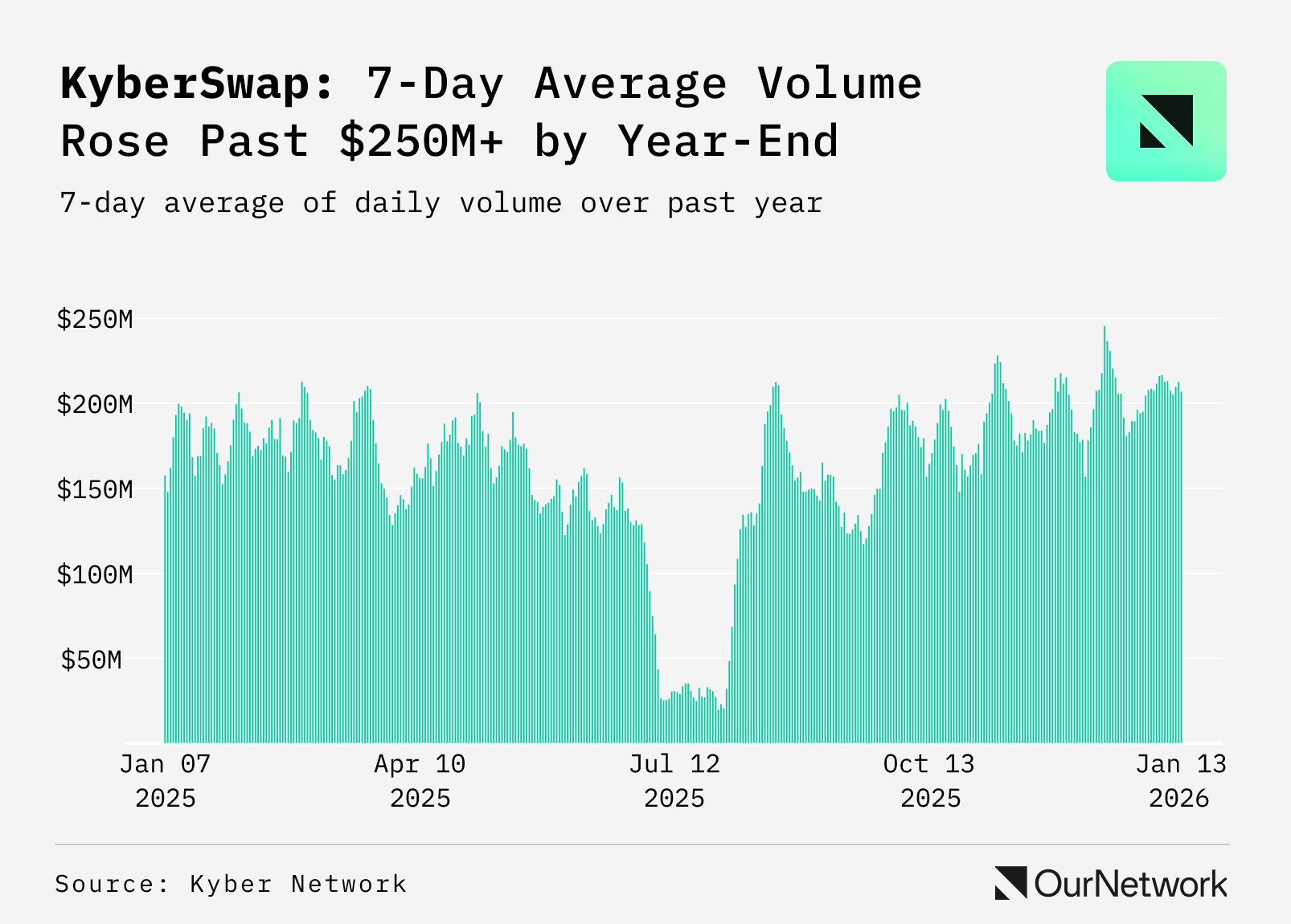

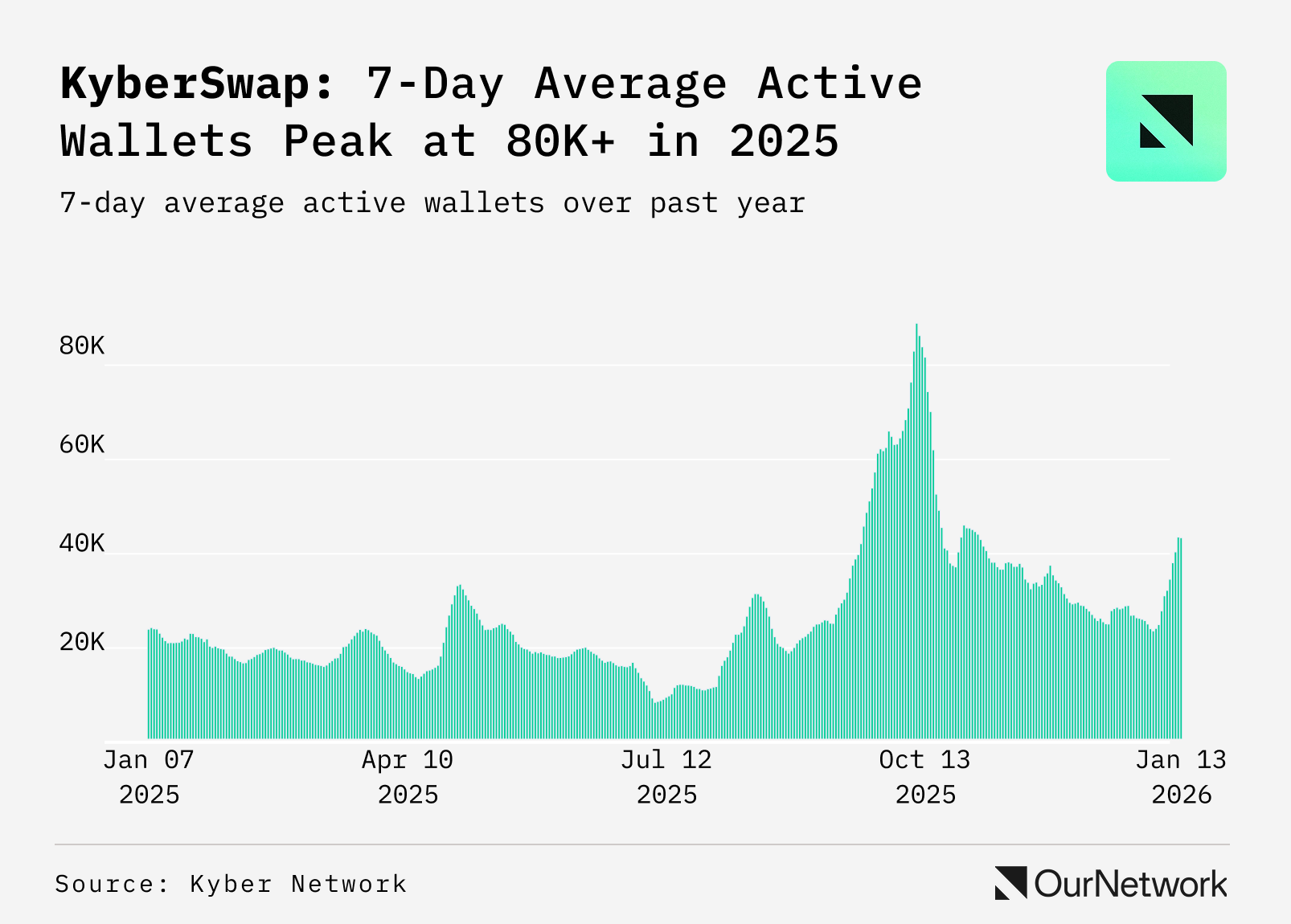

📈 KyberSwap in 2025: Q4 Volumes Stabilized above $150M Per Day, Wallets Decoupled from Volume, and $26B+ Executed Outside of Ethereum Mainnet

- KyberSwap’s 7-day rolling average of daily volume fluctuated throughout 2025, with a mid-year decline coinciding with softer activity across DeFi markets. Despite this slowdown, the rolling average remained above ~$100M for most of the first half of the year. By Q4, the 7-day average consistently moved above ~$150M, indicating a modest but persistent recovery and resilience in execution demand despite broader sector slowdowns.

- Daily unique wallets rose from ~20K in early January to a spike above ~80K in early Q4, then normalized to ~25K–40K. The mid-year volume decline was not matched by a similar drop in wallets, and the wallet spike did not produce a comparable volume peak, showing weak correlation between volume and active wallets.

- Cumulative volume by chain shows Ethereum as the dominant execution venue with $47.3B in traded volume. However, non-Ethereum chains contributed materially, including Base ($9.5B), BNB Chain ($8.0B), Arbitrum ($4.9B), and Avalanche (~$3.9B), highlighting a multi-chain execution profile.